Global Surgical Sutures Market Size 2024-2032

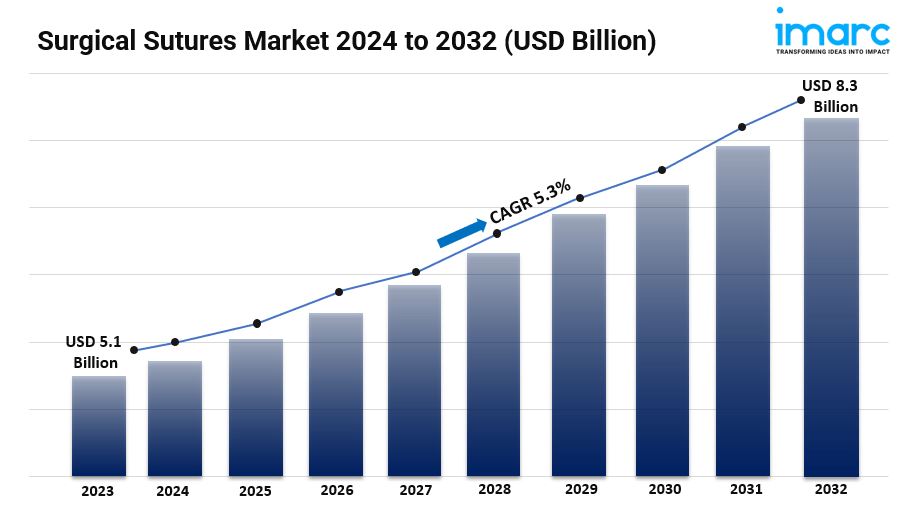

- The global surgical sutures market size reached USD 5.1 Billion in 2023.

- The market is expected to reach USD 8.3 Billion by 2032, exhibiting a growth rate (CAGR) of 5.3% during 2024-2032.

- Absorbable sutures lead the market, accounting for the majority of the surgical sutures market share owing to their gradual dissolution, reducing the need for follow-up procedures.

- Multifilament represents the largest segment due to enhanced tensile strength and flexibility, providing better support during healing.

- Cardiovascular surgeries represent the leading application segment spurred by rising cardiac conditions necessitating intricate surgical techniques and materials.

- Hospitals and clinics hold the largest share in the surgical sutures industry, driven by a high volume of surgical procedures performed daily.

- North America leads the market with its robust healthcare infrastructure and emphasis on innovative medical technologies and practices.

- The growth of the surgical sutures market is driven by an increasing focus on wound care management and infection prevention.

- Additionally, the growing awareness of the importance of surgical outcomes has led to increased investment in training and education for surgical professionals, promoting the adoption of high-quality sutures.

Request to Get the Sample Report: https://www.imarcgroup.com/surgical-sutures-market/requestsample

Industry Trends and Drivers:

- Rising Surgical Procedures:

The increasing prevalence of chronic diseases and injuries necessitating surgical interventions is a primary driver of the surgical sutures market. According to the World Health Organization, the global burden of diseases such as cancer, cardiovascular diseases, and orthopedic conditions is on the rise. As these conditions often require surgical treatment, the demand for effective wound closure solutions, including sutures, has surged.

Additionally, the growing elderly population, which typically has higher surgery rates due to age-related health issues, further propels the demand for surgical sutures. This trend is evident in regions with aging demographics, where surgical procedures for joint replacements, heart surgeries, and cancer treatments are becoming increasingly common.

- Technological Advancements:

The surgical sutures market is significantly influenced by ongoing innovations and advancements in suture technology. Modern sutures are designed with improved materials, such as biodegradable and antimicrobial coatings, which enhance their effectiveness and safety. Innovations like absorbable sutures reduce the need for additional procedures to remove sutures, making them more appealing to both surgeons and patients.

Furthermore, the introduction of advanced suturing techniques, such as minimally invasive surgeries, requires specialized sutures that can accommodate various surgical needs. These technological advancements not only improve patient outcomes but also expand the range of applications for surgical sutures across different types of surgeries.

- Increased Healthcare Expenditure:

Growing healthcare expenditure globally is another critical factor driving the surgical sutures market. Governments and private organizations are investing more in healthcare infrastructure, improving access to surgical services. Enhanced healthcare funding facilitates the procurement of high-quality surgical sutures, thereby boosting their adoption in clinical settings.

Additionally, rising disposable incomes in developing regions contribute to increased spending on healthcare services, including surgical procedures, further driving the demand for surgical sutures. As healthcare systems evolve, the emphasis on patient-centered care also encourages the use of advanced suturing solutions, thereby enhancing market growth.

Speak to An Analyst: https://www.imarcgroup.com/request?type=report&id=4616&flag=C

Surgical Sutures Market Report Segmentation:

Breakup By Type:

- Absorbable Sutures

- Non-Absorbable Sutures

Absorbable sutures dominate the market due to their ability to eliminate the need for removal, enhancing patient comfort and reducing postoperative complications.

Breakup By Material:

- Monofilament

- Multifilament

Multifilament sutures lead the market because of their superior knot security and handling characteristics, making them ideal for complex and high-tension surgical applications.

Breakup By Application:

- Cardiovascular Surgeries

- General Surgeries

- Gynecological Surgeries

- Orthopedic Surgeries

- Ophthalmic Surgeries

- Others

The cardiovascular surgeries segment holds the largest market share due to the increasing incidence of heart-related diseases, necessitating advanced surgical interventions that require effective suturing solutions.

Breakup By End User:

- Hospitals and Clinics

- Ambulatory Surgical Centers

- Others

Hospitals and clinics account for the majority of the market share as they are primary centers for surgical procedures, driving demand for a wide range of suturing options.

Breakup By Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America is the largest market due to advanced healthcare infrastructure, high surgical procedure rates, and significant investment in medical technologies, including surgical sutures.

Top Surgical Sutures Market Leaders: The surgical sutures market research report outlines a detailed analysis of the competitive landscape, offering in-depth profiles of major companies.

Some of the key players in the market are:

- Advanced Medical Solutions Group plc

- B. Braun Melsungen AG

- Boston Scientific Corporation

- CONMED Corporation

- DemeTECH Corporation

- Integra LifeSciences

- Johnson & Johnson

- Medtronic plc

- Mellon Medical B.V.

- Smith & Nephew plc

- Stryker Corporation

- Teleflex Incorporated

- Zimmer Biomet

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact US:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: +1–631–791–1145